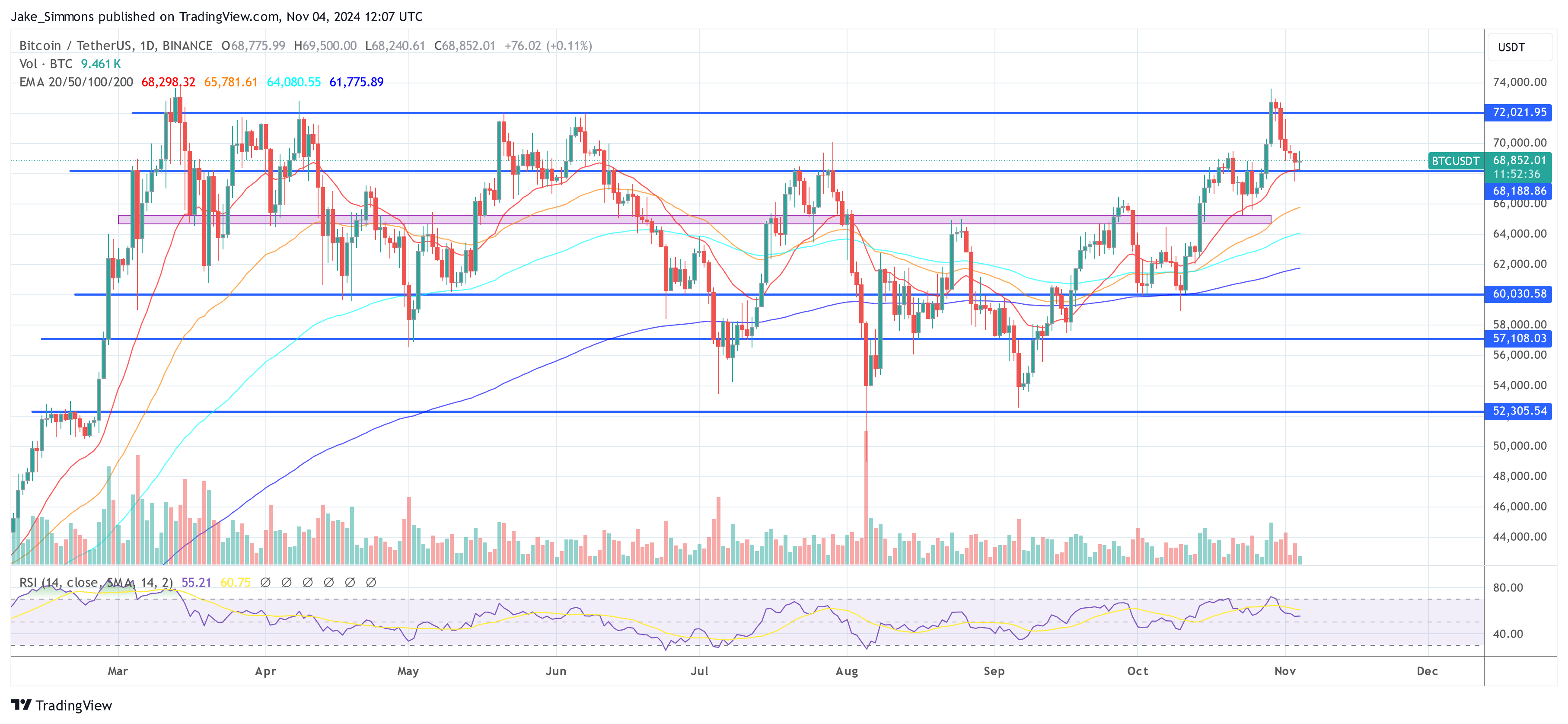

- Bitcoin (BTC) fell over 5% to around $68,779, down from $72,500, in the past 24 hours.

- The defunct Mt. Gox exchange transferred 500 BTC, valued at $35 million, to unknown addresses.

Bitcoin (BTC) dropped to the $69K zone, losing more than 5% in the last 24 hours, following fresh movements of Bitcoin associated with the defunct Mt. Gox exchange. This latest slide comes after BTC traded as high as $72,662, has the crypto world abuzz about what this activity could mean for the market.

According to blockchain analytics firm Arkham Intelligence report on November 1, around 500 BTC, valued at $35 million, was transferred from Mt. Gox-linked wallets to several unknown addresses. Specifically, 1.78 BTC went to one address, while 468.24 BTC ended up in another.

(Source: Arkham)

This is the first large transfer from Mt. Gox-linked wallets in about a month. Still, the wallet was flagged as belonging to Mt. Gox holds an enormous 44,905 BTC—worth roughly $3.12 billion—as per Arkham.

A Glimpse of the Past

This movement comes on the heels of a similar activity in August when Mt. Gox shifted about 13.265K BTC. The transfer worth around $784 million at the time, to an undisclosed wallet. These frequent transfers have raised speculation that Mt. Gox may be preparing for the long-awaited repayment of Bitcoin to its creditors. Originally set for 2024, the platform recently extended its deadline by a year to October 31, 2025.

In May, Mt. Gox firmly denied rumors of a $10 billion BTC and Bitcoin Cash (BCH) selloff from its wallets. However, the current market reaction suggests any movement from these wallets continues to impact Bitcoin’s price. With BTC now trading around $69,567, the day’s trading volume surged over 14% to $44.59 billion.

Mt. Gox, one of the first Bitcoin exchanges, once managed around 70% of all global BTC transactions. But went under in 2014 following significant security breaches. Since then, creditors have eagerly awaited their Bitcoin.