A recent report published by the Bitcoin Policy Institute (BPI) and highlighted by Forbes explores the growing discussion around Bitcoin as a viable reserve asset for central banks.

Authored by Dr. Matthew Ferranti, a Harvard-trained economist and former member of the White House Council of Economic Advisers, presents several compelling arguments for why central banks might consider adding Bitcoin to their portfolios.

Dr. Ferranti begins by noting the trend of central banks increasing their gold reserves, suggesting that Bitcoin could serve as a modern counterpart.

While only one central bank—the Central Bank of El Salvador—has publicly disclosed Bitcoin holdings, Dr. Ferranti highlights that Bitcoin represents just under 10% of El Salvador’s reserves. He argues that an optimal allocation would fall between 2% and 5%, allowing for diversification without excessive risk.

One of the key points raised in the report is Bitcoin’s historical performance during economic crises. Dr. Ferranti argues that a crucial feature of any reserve asset is its ability to provide returns when traditional assets falter.

The report cites examples such as the financial turmoil surrounding the collapse of Silicon Valley Bank in 2023 and the US sanctions on Russia following its invasion of Ukraine in 2022, both of which corresponded with significant spikes in Bitcoin’s value.

Despite Bitcoin’s short-term volatility, Dr. Ferranti posits that it has the potential to outperform traditional assets over longer periods. He attributes this to Bitcoin’s Halving cycle, which reduces the rate of new coin production and can lead to price increases.

Furthermore, the economist notes that both Bitcoin and gold perform well during inflationary periods, suggesting that rising Bitcoin prices might indicate forthcoming inflation.

The report also references findings from the Federal Reserve Bank of New York, which indicate that Bitcoin’s price is largely unaffected by macroeconomic news, except for inflation-related information.

This quality, the doctor says, makes Bitcoin an effective diversifier within a portfolio, especially given its low correlation with traditional reserve assets such as gold and foreign currencies.

Dr. Ferranti outlines three reasons why Bitcoin is devoid of default risk. First, the doctor contends that it does not represent a claim on future cash flows, unlike stocks and bonds.

Second, the network is secured through a robust mining process. Lastly, Bitcoin is immune to financial sanctions—an important consideration for central banks—since it cannot be “frozen” in the same way traditional assets can be.

While acknowledging that Bitcoin does not match the liquidity of the US Treasury market, Dr. Ferranti points out that its liquidity has improved significantly, with a current market cap exceeding $1.3 trillion.

The economist concludes by suggesting that this level of liquidity is adequate for accommodating large transactions, making Bitcoin a more attractive option than in previous years for central banks worldwide.

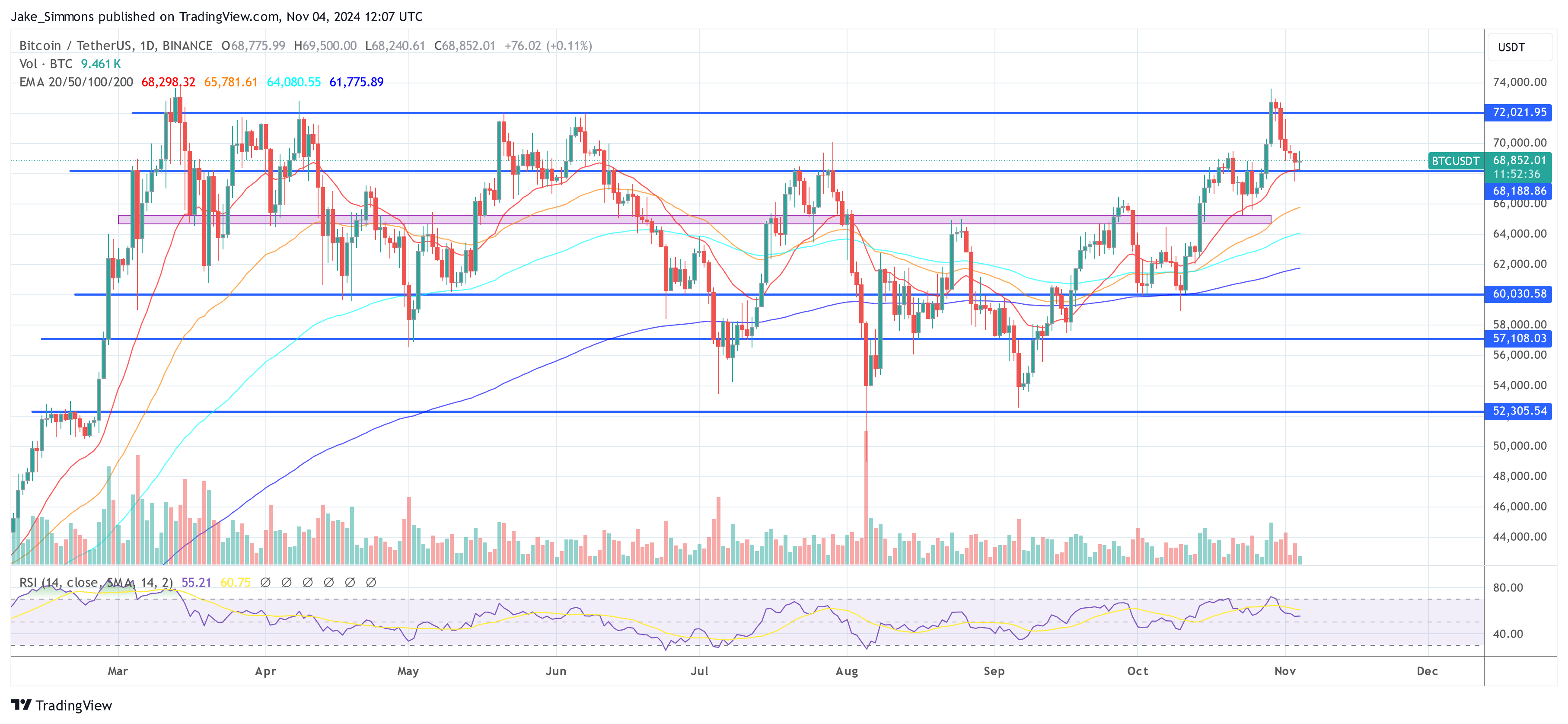

At the time of writing, the largest cryptocurrency on the market is trading at $67,500, down 1.5% in the 24-hour time frame.

Featured image from DALL-E, chart from TradingView.com

Authored by Dr. Matthew Ferranti, a Harvard-trained economist and former member of the White House Council of Economic Advisers, presents several compelling arguments for why central banks might consider adding Bitcoin to their portfolios.

Bitcoin As A Modern Reserve Asset

Dr. Ferranti begins by noting the trend of central banks increasing their gold reserves, suggesting that Bitcoin could serve as a modern counterpart.

While only one central bank—the Central Bank of El Salvador—has publicly disclosed Bitcoin holdings, Dr. Ferranti highlights that Bitcoin represents just under 10% of El Salvador’s reserves. He argues that an optimal allocation would fall between 2% and 5%, allowing for diversification without excessive risk.

One of the key points raised in the report is Bitcoin’s historical performance during economic crises. Dr. Ferranti argues that a crucial feature of any reserve asset is its ability to provide returns when traditional assets falter.

The report cites examples such as the financial turmoil surrounding the collapse of Silicon Valley Bank in 2023 and the US sanctions on Russia following its invasion of Ukraine in 2022, both of which corresponded with significant spikes in Bitcoin’s value.

Despite Bitcoin’s short-term volatility, Dr. Ferranti posits that it has the potential to outperform traditional assets over longer periods. He attributes this to Bitcoin’s Halving cycle, which reduces the rate of new coin production and can lead to price increases.

Furthermore, the economist notes that both Bitcoin and gold perform well during inflationary periods, suggesting that rising Bitcoin prices might indicate forthcoming inflation.

No Default Risk And Immunity To Financial Sanctions

The report also references findings from the Federal Reserve Bank of New York, which indicate that Bitcoin’s price is largely unaffected by macroeconomic news, except for inflation-related information.

This quality, the doctor says, makes Bitcoin an effective diversifier within a portfolio, especially given its low correlation with traditional reserve assets such as gold and foreign currencies.

Dr. Ferranti outlines three reasons why Bitcoin is devoid of default risk. First, the doctor contends that it does not represent a claim on future cash flows, unlike stocks and bonds.

Second, the network is secured through a robust mining process. Lastly, Bitcoin is immune to financial sanctions—an important consideration for central banks—since it cannot be “frozen” in the same way traditional assets can be.

While acknowledging that Bitcoin does not match the liquidity of the US Treasury market, Dr. Ferranti points out that its liquidity has improved significantly, with a current market cap exceeding $1.3 trillion.

The economist concludes by suggesting that this level of liquidity is adequate for accommodating large transactions, making Bitcoin a more attractive option than in previous years for central banks worldwide.

At the time of writing, the largest cryptocurrency on the market is trading at $67,500, down 1.5% in the 24-hour time frame.

Featured image from DALL-E, chart from TradingView.com